Almost every Will written in Ontario, and indeed in most jurisdictions, begins with the phrase or something close to it “I hereby revoke all Wills and testamentary dispositions of every nature and kind whatsoever made by me before”.

To the average person this simply means that any previous Will you made is canceled and replaced with your new will. However, a testamentary disposition is far wider than a Will. It speaks of what is to occur with respect to any asset upon one’s death. Think about that. That includes insurance policies, beneficiary designations in RRSPs and potentially placing a property in joint tenancy with right of survivorship.

The average person would think that the only way to change a beneficiary designation in a RRSP or life insurance policy would be by changing that beneficiary designation at the very institution where the insurance policy or RRSP was held. That is not the case. The Ontario Succession Law Reform Act sections 51 and 52, permit beneficiary designations and indeed changes and revocations to be made in one’s Will.

One must be very careful. Generally in the Wills that we draft they contain a provision whereby their spouses are often named as their beneficiary of assets such as RRSP or TFSA.

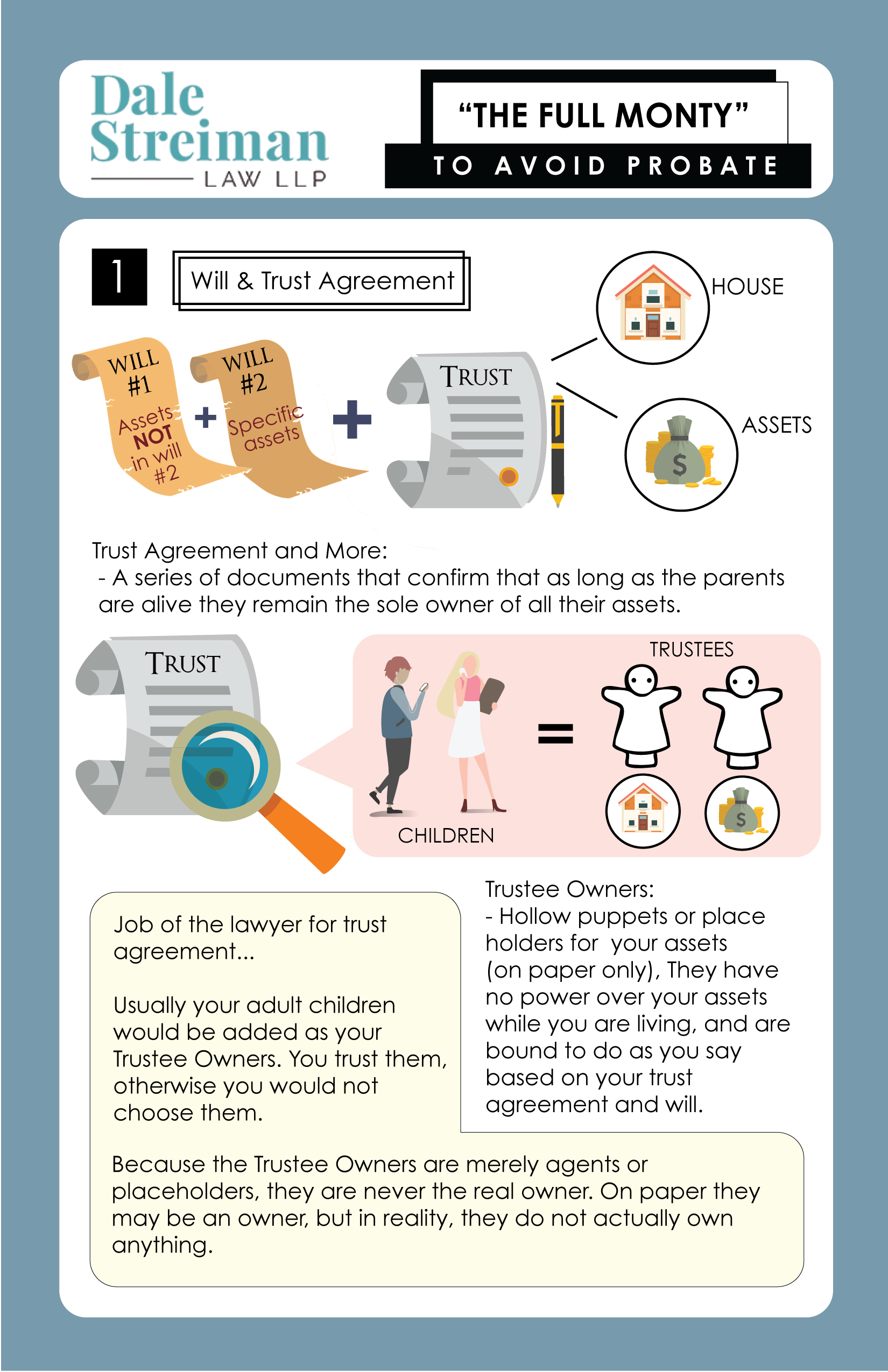

When the “Full Monty” process is undertaken, this is not the case and we carefully must ensure that there is a consistent approach. For information about the Full Monty simply use that search term on our website.

So what is the law in Ontario and indeed across Canada when we have a standard Will with a revocation/cancelling clause at the start of one’s Will when there is a prior beneficiary designation for registered assets such as an RRSP or TFSA?

In the 2021 decision by the Honourable Madame Justice Catriona Verner of Alger v. Crumb, a decision of the Ontario Superior Court of Justice, this very question was debated.

It is interesting to note that Justice Catriona Verner had only been sitting on the bench approximately a year when she released her decision. Justice Verner came to the court with a very serious criminal law background, but not one in civil law and certainly not Wills and Estates. Nonetheless, her legal intellect was brought to bear in this decision and the author heartily agrees with the decision that she reached.

Alger v. Crump is a case dealing with a small estate. But the fact situation is almost universal and as such is an important decision. It reviews the law as this issue has come up a number of times across Canada. If your Will says I revoke my earlier testamentary dispositions, and a beneficiary designation of an RRSP is a testamentary designation, does that mean it’s canceled, does that mean the RRSP now forms part of the estate?

In this decision, Justice Verner had before her a number of decisions holding different positions across the country. She had the decision of Justice McIssac in McNaughton Automotive v. The Co-operators General Insurance. We discussed in another blog article how that decision was clearly wrong. WHAT HAPPENS WHEN A JUDGE IS WRONG?

Justice Verner closely looked at sections 51 and 52 the Succession Law Reform Act. She also looked at the Ontario Court of Appeal decision in LaCzova Estate v. Madonna House.

The law as concluded by Justice Verner is that it is not enough to make a general sweeping statement revoking all testamentary dispositions. To meet the provisions of the Succession Law Reform Act, the specific asset such as a RRSP, life insurance policy, RIF or a TFSA must not only be specifically referred to, but also the beneficiary designation that is now being changed must also be stated. Failure to do so means a general statement found at the opening of every Will has no effect.

Common sense, good law.

One must be very careful and appreciate the effect of standard clauses contained in Wills across the land. In Nova Scotia, there is no equivalent to sections 51 and 52 of the Succession Law Reform Act. Accordingly in Nova Scotia, such a general opening phrase will cancel an earlier beneficiary designation.

Quite frankly this demonstrates, that using a Will kit or having a Will prepared by a lawyer that does not specialize in Wills and Estates can be an example of playing with fire.